{kind=link}

The Question Nobody Thinks to Ask Before Buying a Policy

You sit down with a car insurance agent. They’re friendly, knowledgeable, and genuinely seem to be helping you find the best deal. But in the back of your mind, one question keeps quietly surfacing: Is this person getting paid to sell me something specific?

It’s a fair — and smart — question. And the honest answer is yes.

Car insurance agents do get commissions. That’s how most of them make their living. But the details — how much, from whom, and what it really means for your wallet — are things most buyers never think to investigate.

Here are 7 shocking truths about car insurance agent commissions that every policyholder deserves to know.

Shocking Truth #1: Yes, Car Insurance Agents Do Get Commission — On Every Policy

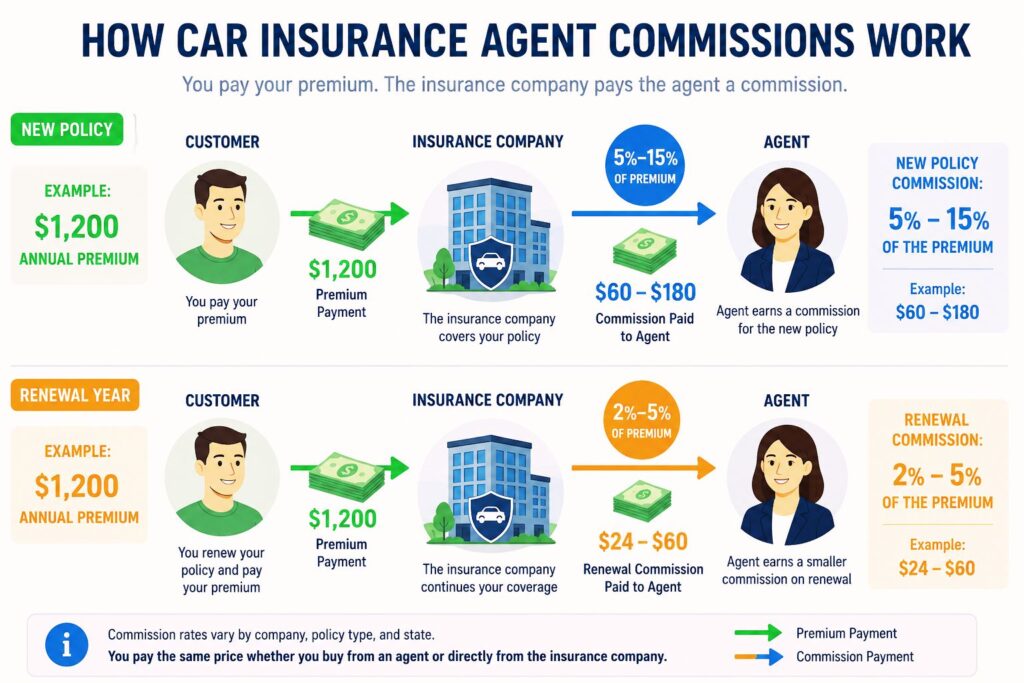

Let’s settle this straight away. The vast majority of car insurance agents are paid a commission based on the premiums of the policies they sell — on every single policy.

According to AutoInsurance.org, auto insurance agents typically earn 10% to 15% in commissions, though the full range runs anywhere from 5% to 20% depending on agent type, carrier, and coverage.

The commission comes out of the premium the insurance company collects. You pay $1,200 a year for car insurance — a portion flows directly to the agent who sold or manages your policy. The rest covers claims, underwriting, administration, and the insurer’s profit margin.Crucially, as ALLCHOICE Insurance explains, you don’t pay the agent directly. The insurance carrier pays them automatically from your premium. From your side of the desk, you write one check — and everything else happens behind the scenes, whether you know it or not.

Shocking Truth #2: Your Agent Gets Paid Again Every Year You Renew

Most buyers assume the agent gets paid once — when they sell the policy. The reality is more lucrative than that.

When you renew your policy the following year, your agent earns another commission. These renewal commissions typically run between 2% and 5%, according to Insurance Business Magazine.

That may sound modest, but consider this: an agent with 500 active clients renewing at an average premium of $1,200 per year, earning just 3% on each renewal, is generating $18,000 in passive income — without selling a single new policy that year.

This is why experienced agents with large client books often have renewal income that covers a significant chunk of their living expenses before they’ve made their first new sale of the year. It’s a business model quietly built for the long game — and your annual renewal is a big part of it.

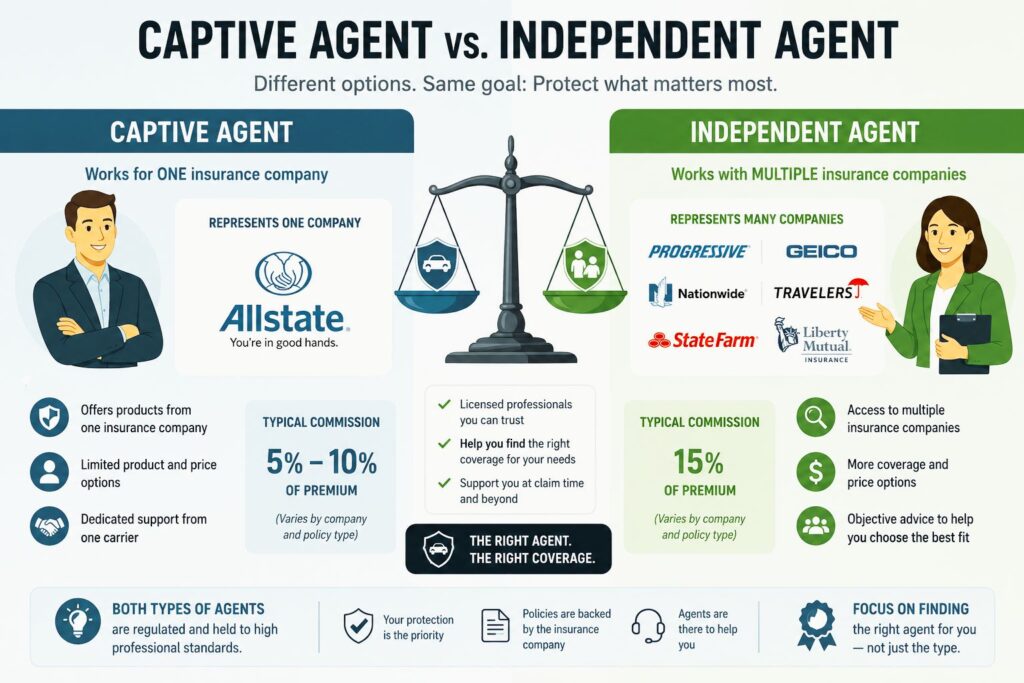

Shocking Truth #3: Captive and Independent Agents Earn Very Different Commissions

Not all agents are created equal — and neither are their paychecks. The type of agent you work with dramatically changes how much commission they earn and what options they can actually offer you.

Captive agents work exclusively for one insurance company — think State Farm, Allstate, or Farmers. They typically earn 5% to 10% of the first year’s premium on auto policies.

Independent agents represent multiple carriers and can shop your risk across the open market. They generally earn around 15% on new auto policies, according to Insure.com.

Here’s the full picture side by side:

| Feature | Captive Agent | Independent Agent |

|---|---|---|

| Works for | One insurer only | Multiple carriers |

| New policy commission | 5%–10% | ~15% |

| Renewal commission | 2%–5% | 2%–5% (varies) |

| Base salary | Often yes | Rarely |

| Benefits (health, 401k) | Usually included | Self-funded |

| Business expenses | Covered by carrier | Paid out of pocket |

| Policy options for you | Limited to one carrier | Broad market access |

| Earning ceiling | Capped | Uncapped |

Sources: Insure.com, Aceable Insurance

The trade-off is real. Captive agents offer brand familiarity and stability. Independent agents offer market-wide comparison and potentially better rates — but carry their own overhead. Neither is automatically the better choice; it depends entirely on what you value most.

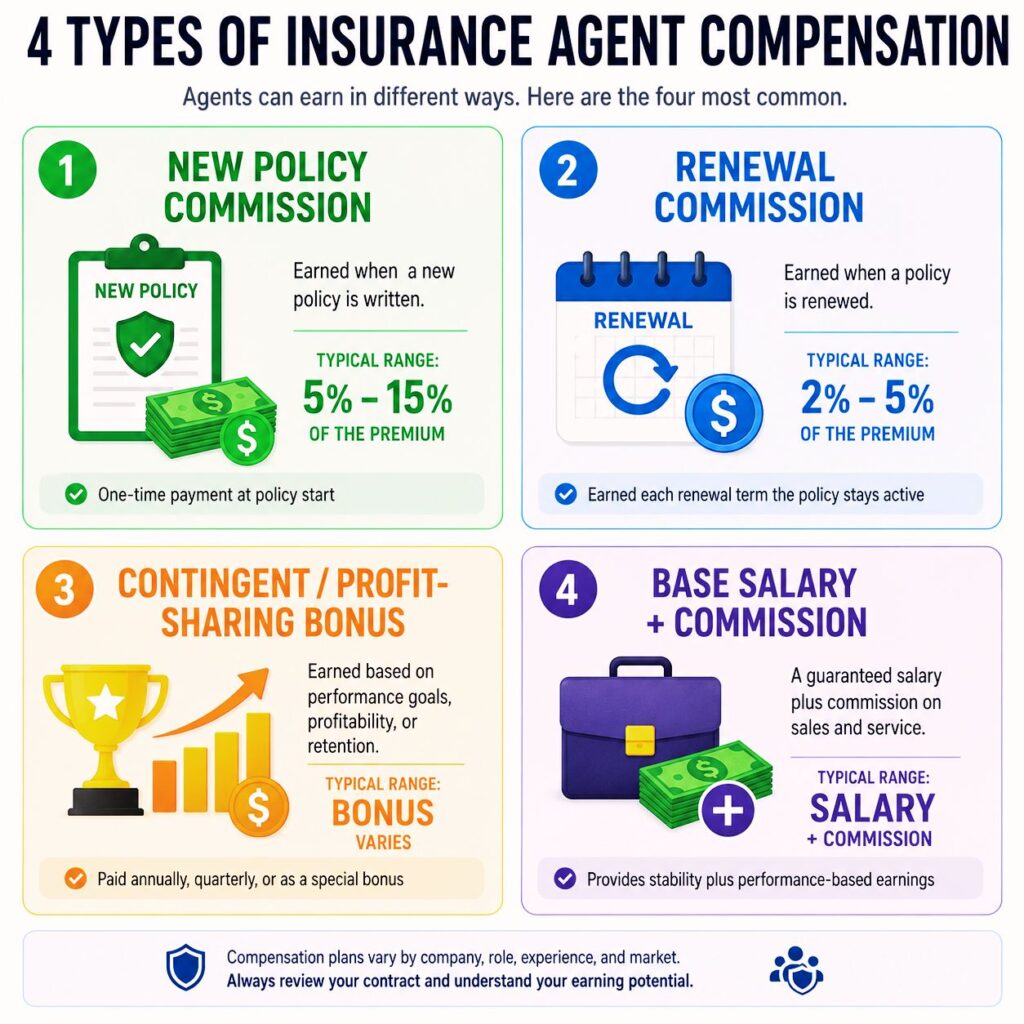

Shocking Truth #4: There Are 4 Different Ways Agents Get Paid — Not Just One

Most people assume agents simply earn a cut of your premium. The reality is more layered — and understanding all four compensation types helps you see the full picture.

1. New Business Commission

The biggest single payout. Paid every time an agent sells a brand-new policy. For auto insurance, this is typically 5%–15% of the first year’s premium, depending on agent type.

2. Renewal Commission

Paid every year the policy stays active. Lower than the new policy rate — usually 2%–5% — but it stacks significantly over time across a large client base.

3. Contingent Commissions (Profit-Sharing Bonuses)

Many carriers reward agencies that hit performance targets — such as volume thresholds, high retention rates, or low claims ratios. According to Huff Insurance, these profit-sharing bonuses typically add around 1% to 2% of total written premiums on top of regular commissions.

4. Base Salary Plus Commission

Common among captive agents at large carriers. Many receive a modest base salary — often in the $35,000–$50,000 range according to Aceable Insurance — supplemented by commissions and performance bonuses. This provides income stability while still incentivizing sales.

Shocking Truth #5: Car Insurance Agents Can Earn Over $135,000 a Year

The income potential in this career surprises most people. This isn’t just a mid-level sales job.

According to the most recent data from the U.S. Bureau of Labor Statistics (BLS), insurance sales agents earn a median annual wage of $60,370. The bottom 10% earn under $36,390, while the top 10% bring in over $135,660 per year.

It’s worth noting: the BLS wage data doesn’t fully capture commission earnings. Total real-world compensation is typically higher. ZipRecruiter data cited by Agency Height puts the average annual pay for a licensed insurance agent at $69,998 as of early 2026, factoring in commissions and bonuses.

| Earning Tier | Annual Income |

|---|---|

| Bottom 10% | Under $36,390 |

| 25th Percentile | ~$31,500–$43,000 |

| Median | ~$60,370 |

| 75th Percentile | ~$75,500 |

| Top 10% | Over $135,660 |

Sources: BLS Occupational Outlook, Insurance Business Magazine

The agents at the top of that range aren’t just lucky — they’ve spent years building a large, loyal client base where renewal commissions alone generate substantial passive income every single month.

ALSO READ: How to Start an Electronic Music Career in 2026

This is the one most agents won’t volunteer. And it’s backed by independent research.

A study by the Consumer Federation of America found that insurance companies paying higher commissions tend to charge above-average premium rates — without providing better service or higher customer satisfaction.

The numbers are striking: insurers with below-average auto insurance rates paid agents an average commission of 3.9%. Insurers with above-average rates paid an average commission of 7.7%.

That said, you don’t pay the agent separately. As ALLCHOICE Insurance points out, having an insurance agent doesn’t affect your premium in a direct line-item sense. The commission is priced into the carrier’s model. But choosing a high-commission carrier can indirectly mean you’re paying more — without getting more coverage or better service in return.

The smart move: compare quotes across both high-commission carriers and low-commission or direct-to-consumer insurers. The Consumer Federation of America specifically recommends getting at least one quote from a low-commission direct writer during every insurance shopping session.

Shocking Truth #7: You Have the Right to Ask Your Agent About Their Commission

Most buyers never think to ask. But in many states, you’re fully entitled to know — and in some, agents are legally required to tell you.

New York’s Insurance Regulation 194 requires agents and brokers operating in the state to disclose commission rates and any year-end carrier bonuses if a customer asks. Even in states without that specific mandate, a transparent and ethical agent should answer this question directly and without hesitation.

These are the questions every buyer should feel empowered to ask:

- What commission rate are you earning on this policy?

- Are you recommending this carrier because it’s the best fit for me, or because it pays you more?

- What other carriers do you represent, and what would I pay with each of them?

- Do you receive any contingent bonuses or profit-sharing from the carrier you’re recommending?

You’re not being confrontational by asking these questions. You’re being an informed consumer — and any agent worth your business will respect that entirely.

What This Means for You as a Car Insurance Buyer

Understanding how your agent gets paid isn’t about distrust. It’s about making smarter, more confident decisions. Here’s how to put all 7 truths to practical use:

Shop multiple sources. Get quotes from both agent channels and direct-to-consumer platforms. Include at least one low-commission direct writer in every comparison to get a full picture of the market.

Review your policy annually. Don’t let it auto-renew on autopilot. An annual review catches coverage gaps, newly available discounts, and whether your current carrier is still competitive.

Value great agents — they earn their commission. A skilled independent agent who shops your risk across 15 carriers, explains your coverage clearly, and handles your claims professionally is worth every dollar of their commission. The commission isn’t the problem; uninformed buying is.

Expert Tips: Getting the Most Value When Working With a Car Insurance Agent

Expert Tip #1: Ask an independent agent to show you side-by-side quotes from at least three different carriers. If they can only produce one or two options, find someone with broader market access.

Expert Tip #2: Review your policy every year at renewal — not just the price, but the coverage details. Commission-motivated agents may let a policy auto-renew without flagging gaps or newly available discounts.

Expert Tip #3: Don’t assume buying directly online is always cheaper. Many direct insurers pour money into TV advertising — those costs are built into premiums too. Compare total value, not just the sticker price.

Expert Tip #4: If an agent recommends add-on coverage you didn’t ask about, ask them to explain specifically why you need it. More coverage means a higher premium — and a higher commission. The advice may still be sound, but you deserve the full reasoning.

Expert Tip #5: Work with agents who ask questions before quoting. An agent who understands your driving habits, vehicle use, and financial situation before making recommendations is doing their job right — and worth every dollar of their commission.

Pros and Cons of Buying Through a Commission-Based Agent

| Pros | Cons |

|---|---|

| Expert guidance on coverage options | Agent may favor higher-commission policies |

| Independent agents shop multiple carriers | No guaranteed unbiased recommendation |

| Ongoing relationship for claims and renewals | Commission structure isn’t always transparent |

| Can find specialized or hard-to-place coverage | Some agents may oversell add-ons |

| Typically no out-of-pocket cost to you | High-commission carriers can mean higher premiums |

Frequently Asked Questions

1. Do car insurance agents get commission on every policy they sell?

Yes. In most cases, car insurance agents earn a commission on every new policy they sell and a smaller renewal commission each year the policy stays active. The exact percentage depends on whether they’re a captive or independent agent and which carrier the policy is with. According to AutoInsurance.org, commissions typically average 10%–15%, with a full range of 5%–20%.

2. Does the commission my agent earns make my car insurance more expensive?

Not in a direct, itemized way — you don’t pay a separate agent fee. The commission is built into the carrier’s pricing model. However, research from the Consumer Federation of America shows that carriers paying higher agent commissions tend to charge above-average rates — so there is an indirect relationship worth knowing about.

3. What’s the difference between a car insurance agent and a broker?

An insurance agent represents one or more insurance companies and sells their products. A captive agent works for one carrier; an independent agent works with many. An insurance broker legally represents the buyer — not the insurer — and can compare across the market but typically needs to work through an agent or carrier to actually bind coverage. Both earn commissions. The BLS reports insurance brokers earn a median of about $59,580 per year.

Not directly — commission rates are set by the carrier’s contract with the agent, not negotiable by the buyer. However, you can absolutely work with your agent to lower your overall premium by identifying discounts, adjusting coverage levels, raising your deductible, or comparing quotes across carriers. An independent agent with broad market access has far more tools to reduce your cost than a captive agent locked into one company.

5. Should I buy car insurance directly online to avoid paying agent commissions?

Not necessarily. Direct-to-consumer insurers that bypass agents often spend heavily on advertising and technology — costs that flow back into premiums anyway. You also lose personalized coverage advice, annual policy reviews, and hands-on claims support. The Consumer Federation of America recommends comparing both direct writers and agent-based carriers to find the best mix of price and service for your specific situation.

Conclusion: Commission Isn’t a Red Flag — But Knowing the Truth Is Power

Car insurance agents earn commissions. That’s not a scandal — it’s simply how the industry works, and when the model functions well, it aligns everyone’s interests. Your agent gets paid when you’re happy and when you stay. That’s not a bad thing.

What matters is that you now know the full picture: the percentages, the renewal income stream, the difference between captive and independent agents, the hidden profit-sharing bonuses, and the research linking high commissions to higher premiums.

A buyer who understands these 7 shocking truths walks into every insurance conversation with a clear advantage — and that knowledge is worth far more than any commission your agent will ever earn.